April 2, 2026 · BTCD Team

USD Vault: How the Engine Works

Vault Architecture & Yield Mechanics

The Bitcoin Dollar USD Vault

The USD Vault is a dollar-denominated yield product that targets 12–14% net APY on USDC deposits by deploying capital through a structured leveraged position in sBTCD — the yield-bearing Bitcoin Dollar token. This document details the construction of that vault: how capital flows in, how yield is generated and managed, and how the position is maintained and unwound.

Target Structure

- Deposit asset: USDC

- Buffer asset: sUSDS

- Network: Ethereum mainnet

- Target net APY: 12–14%

- Yield engine: 2× leveraged sBTCD position

- Execution infrastructure: Morpho isolated lending pools, flash loans

- Rebalancing: Passive through internal RFQ/Coincidence of Wants

The Building Blocks: sBTCD

Everything in the USD Vault flows from a single underlying instrument: sBTCD, the yield-bearing form of the Bitcoin Dollar token.

sBTCD is minted when users stake BTCD — the base token of the Bitcoin Dollar protocol. The underlying BTCD portfolio holds approximately 50% Bitcoin assets and 50% USD assets at all times. By staking, users transition from holding the base token to holding a claim on the yield that portfolio generates.

Over time, 1 sBTCD represents a progressively larger amount of BTCD as yield accrues into the staking contract. The vault realizes yield through the appreciation of sBTCD.

Where sBTCD Yield Comes From

sBTCD yield has two sources, ordered by significance:

- Productive asset allocation: Both the BTC and USD sleeves of the underlying portfolio are deployed into yield-generating strategies — dollar-denominated yield instruments and Bitcoin-denominated yield instruments.

- Volatility monetization: The portfolio maintains a banded ~50/50 BTC/USD target. As Bitcoin's price fluctuates, the portfolio systematically rebalances — buying low and selling high in a manner structurally analogous to volatility harvesting in traditional alternatives. This generates additional return on top of productive asset yield.

Yield Smoothing

Rather than distributing yield as earned daily, each 24-hour payout reflects a trailing average of yield earned. Two effects follow:

- Predictable distributions — payouts do not spike or compress with short-term market conditions.

- Structural overcollateralization — because yield is distributed with a lag relative to what is earned, the protocol holds a persistent buffer of accrued-but-undistributed yield. This buffer provides a natural safety margin.

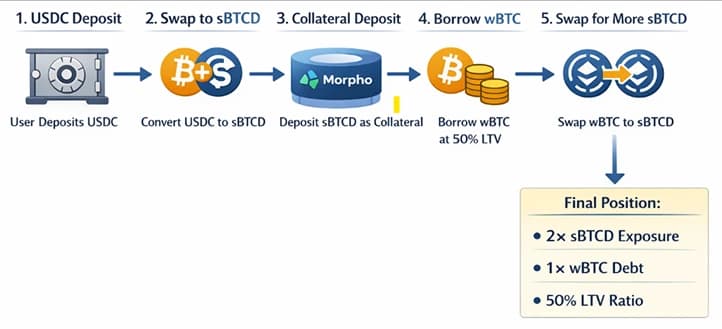

Capital Flow: Deposit to Position

From a single USDC deposit, the vault executes the following sequence to achieve 2× leveraged sBTCD exposure with BTC-neutral net positioning:

- User deposits USDC into the USD Vault.

- Vault mints or swaps USDC into sBTCD — the yield-bearing Bitcoin Dollar staking token, backed by a portfolio of ~50% BTC and ~50% USD assets.

- sBTCD is deposited as collateral into a Morpho isolated lending pool.

- Vault borrows wBTC against that collateral, targeting a 50% loan-to-value (LTV) ratio — $100 of BTC debt against $100 of initial sBTCD collateral.

- Borrowed wBTC is swapped into additional sBTCD, which is deposited as additional collateral.

- Final position: ~2× sBTCD exposure, ~1× wBTC debt, at 50% LTV.

Why USD-Neutral?

sBTCD itself holds approximately 50% BTC and 50% USD. The vault's debt is denominated entirely in BTC (wBTC). These two exposures offset: the BTC component of the collateral is matched by BTC-denominated debt, leaving the net position USD-denominated with no directional Bitcoin price risk.

Yield Architecture

The 2× Leverage Multiplier

The core mechanic is straightforward: by achieving 2× sBTCD exposure through collateral leverage, the vault earns sBTCD yield on twice the user's deposited capital. If sBTCD yields 10% APY, the net yield is estimated to be between 12-14%.

| Component | Rate |

|---|---|

| sBTCD base yield | ~8% APY |

| × 2 leverage factor | = 16% gross |

| Less: wBTC borrowing cost | ~2–3% APR |

| Less: rebalancing friction (estimated) | ~0–2% |

| Net Target APY | 12–14% |

LTV Management and Rebalancing

Maintaining the target 50% LTV is the primary operational challenge of the vault. As Bitcoin's price moves, the value of both the sBTCD collateral and the wBTC debt shifts, pushing the LTV away from target. The vault must rebalance to restore it.

When Bitcoin Price Rises

The sBTCD collateral increases in value while the wBTC debt increases in value faster, causing LTV to increase above target. The vault de-levers:

- Sells a portion of sBTCD collateral.

- Acquires wBTC to repay a portion of the debt.

- LTV returns toward 50%.

When Bitcoin Price Falls

The sBTCD collateral loses value in USD terms, and the portfolio's internal rebalancing mechanism must purchase additional BTC to maintain its ~50/50 target — buying into a falling asset. Simultaneously, the wBTC debt becomes cheaper in USD terms as Bitcoin's price declines, causing LTV to fall below target. The vault releverages:

- Borrows additional wBTC.

- Swaps wBTC into more sBTCD.

- Deposits as additional collateral, restoring 50% LTV and increasing yield-bearing exposure.

When a User Wants to Withdraw

When a user withdraws from the USD Vault, the vault unwinds its leveraged position atomically — flash-borrowing wBTC to repay its outstanding debt and releasing the underlying sBTCD collateral. The released sBTCD is retired against the BTCD Portfolio, redeeming USDC to be returned to the user. The full unwind executes in a single transaction with no cooldown period and no reliance on secondary market liquidity.

The Internal Liquidity Engine

The largest source of friction in any leveraged vault strategy is the cost of executing rebalancing trades on external markets — slippage, fees, and MEV exposure compound against yield over time. The BTCD ecosystem is designed to eliminate most of this friction through an internal matching mechanism.

How the Internal RFQ Works

The BTCD Portfolio — the underlying assets that back all BTCD tokens — maintains a tight ~1% tolerance around its own 50/50 BTC/USD target, meaning it rebalances frequently and in small increments. When Bitcoin's price moves, the Portfolio and the USD Vault almost always find themselves on opposite sides of the same trade:

- A Bitcoin price rise triggers the Portfolio to sell BTC (rebalancing down its BTC allocation) — while simultaneously triggering the USD Vault to acquire BTC with sBTCD (to repay wBTC debt and deleverage).

- A Bitcoin price fall triggers the Portfolio to buy BTC — while the USD Vault needs to borrow more wBTC to acquire sBTCD (to re-lever).

Rather than both sides independently going to external markets, the protocol internalizes these trades:

- The Portfolio broadcasts a trade intent at current market rates.

- The Vault evaluates whether the offered price moves its LTV toward target. If it does, the Vault accepts.

- The swap executes internally, bypassing all external AMMs. Zero slippage. No third-party fees. No MEV exposure.

Critically, this internal execution also grants the vault special permission to bypass the standard 7-day sBTCD cooldown period — enabling instantaneous rebalancing that is not available to external participants. The portfolio can mint BTCD or retire BTCD when it trades with the vault which rebalances the portfolio in the desired direction.

Safety Valve

If no internal match is available — because the Portfolio and Vault are not on opposite sides of a trade, or the offered price does not improve the Vault's LTV — the vault defaults to external execution at the best available market price. System stability does not depend on internal matching being available.

Scale Dynamics

Vault TVL growth by definition creates TVL growth within the BTCD Portfolio ensuring that as the trade size for Vault re-leveraging and deleveraging grows, the BTCD Portfolio will also be offering larger trades. The vault only accepts trades that move it closer to its 50% LTV objective and at a better price than is available anywhere else. The BTCD Portfolio has tighter rebalancing constraints than the vaults so tends to want to trade more frequently meaning the vault is constantly seeing offers and only trades which are mutually beneficial occur.